Retirement planning means you turn today’s income into future monthly income. You estimate what you need each month after work stops, then build savings and investments to match that number. In Malaysia, EPF sits at the centre of this plan because most employees contribute every month through payroll. EPF retirement planning works best when you treat EPF as an income tool, not a lump sum to spend.

A simple starting point helps you move fast. Write down your expected retirement age, your monthly spending target and how long you want your money to last. Many Malaysians plan for about 20 years of retirement income because people live longer than before. EPF built its newer guidance around a 20-year drawdown idea to match life expectancy patterns.

EPF Retirement Planning in Malaysia: How EPF Contributions Build Your Base Investment

EPF retirement planning begins with consistent contributions. EPF collects contributions from employees and employers, then invests the pool to generate annual dividends. For many employees under 60, a common reference point is an employee rate of 11 per cent and an employer rate that often sits at 12 per cent or 13 per cent, depending on wages. These rates matter because small percentage differences compound across decades.

Treat your EPF contribution for retirement as a non-negotiable bill. When your salary rises, your contribution amount rises too, so you save more without changing habits. If you receive bonuses or commissions, build a separate plan to top up so your retirement pace keeps up with lifestyle costs. EPF allows voluntary contributions for some member groups, so you can add more when cash flow improves.

Understanding the EPF Three-Account Structure and How It Affects Your Future

EPF retirement planning changed after EPF moved to a three-account structure. New contributions allocate 75 per cent to Akaun Persaraan, 15 per cent to Akaun Sejahtera and 10 per cent to Akaun Fleksibel. This structure shapes how much stays locked for retirement versus how much stays available for life needs.

Akaun Persaraan drives your retirement outcome, so protect it. Akaun Sejahtera supports planned needs like housing, education and health-related goals, so use it with a clear rule. Akaun Fleksibel gives short-term access, so you need discipline to stop small withdrawals from turning into a habit. If you withdraw from Flexibility often, your future monthly income drops because you cut the money that would earn dividends for years.

EPF Withdrawal Rules in Malaysia: Smart Retirement Planning at Age 55 and Age 60

EPF withdrawal rules in Malaysia affect how long your money lasts. Many members focus on age 55 because EPF provides access routes around that milestone, then age 60 matters for later stage planning. Your decision at retirement matters as much as your savings total because spending speed decides whether funds last. EPF encourages a monthly drawdown idea to support income over time instead of a fast lump sum exit.

Build a simple withdrawal rule before you retire. Set a monthly amount, review it once a year and keep a cash buffer outside EPF for medical or family shocks. If you plan a lump sum, split it into buckets with clear jobs, such as one bucket for one year of expenses, one for health coverage and one for longer-term investments. This approach reduces the risk of overspending in the first two years of retirement.

Understanding RIA Savings Targets and Retirement Income Benchmarks

EPF retirement planning now uses a Retirement Income Adequacy framework with three savings levels. EPF anchors the Adequate level at RM650,000 at retirement age, the Basic level at RM390,000 and the Enhanced level at RM1.3 million. EPF links these levels to a 20-year drawdown approach, so the number connects to income, not ego.

EPF also linked this framework to Belanjawanku guidance and a reference monthly cost for a senior single person. EPF cited about RM2,690 per month as an adequate retirement income reference in the Klang Valley context, then used 240 months to build the RM650,000 benchmark. This helps you translate a big savings number into a monthly spending plan you can understand and measure.

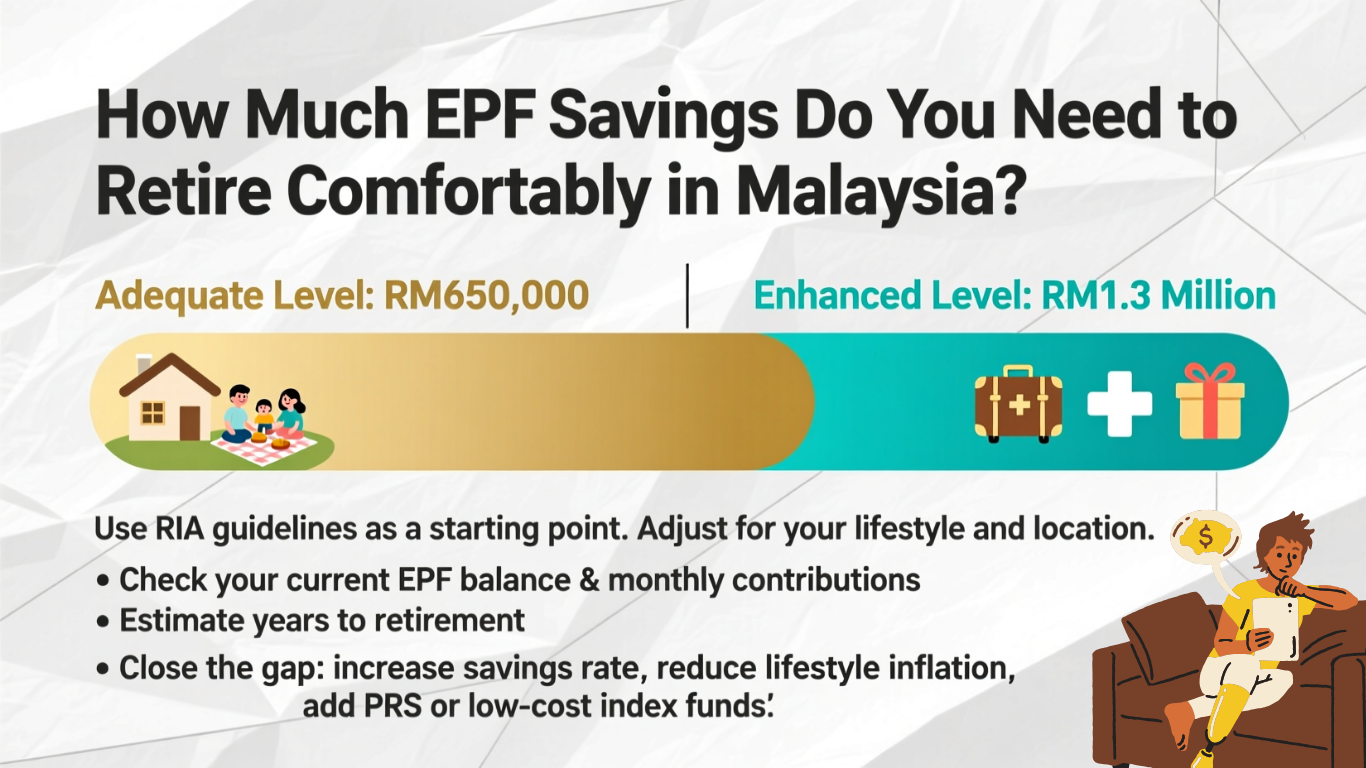

How Much EPF Savings Do You Need to Retire Comfortably in Malaysia?

Many people ask, how much EPF is needed to retire comfortably. Use the RIA levels as your first answer, then adjust for your real expenses and location. If you target a reasonable standard of living, the Adequate savings level of RM650,000 gives a clear planning target. If you want more flexibility for travel, health costs and family support, the Enhanced level of RM1.3 million gives a wider margin.

Now turn the target into actions. Check your EPF balance, your monthly contribution amount and your years left to retirement. If the gap looks big, raise your savings rate, reduce lifestyle inflation and add a second retirement pillar such as PRS or low-cost diversified investments. Keep the plan simple, then repeat it each year.

Exploring the Best Retirement Plans Beyond EPF

Many readers ask, what are the best retirement plans in Malaysia. EPF gives stability and structure, but you need a second pillar if you want a higher retirement income or earlier retirement. A common complement is the Private Retirement Scheme, which allows voluntary contributions and fund choice under a regulated structure. Add simple diversified investments for growth, such as broad-based funds, plus a cash buffer for emergencies.

Build your plan around roles. Use EPF as your core retirement income base. Use PRS or lasting investments for extra growth and tax planning if it fits your situation. Use an emergency fund and insurance so you avoid pulling retirement money for temporary shocks. This structure answers the biggest failure point in retirement planning, which is early leakage of enduring savings.

Final Thought: A Simple Action Plan For The Next 30 Days

Log in to your EPF account, record your Akaun Persaraan balance and record your monthly contribution amount. Then choose one RIA target level as your next milestone: Basic, Adequate or Enhanced. Use the target to decide how much extra you need per month to close the gap.

Next, lock in one behaviour change. Set an automatic transfer into savings on payday so your retirement plan runs without daily decisions. If you earn variable income, commit a fixed percentage of every invoice to retirement savings. Then schedule a yearly review date, so you can track progress and adjust early. EPF retirement planning rewards steady action more than complex tricks.

Unlock Your Wealth Management with HWG Asia – Malaysia’s Leading Wealth Management Partner

Explore more with HWG

HWG is a Malaysia-based wealth education and marketing support platform that partners with licensed financial institutions. We share practical insights and coordinate services delivered by appropriately licensed entities within our group (e.g., Maxima Advisory).

We focus on education and coordination across topics like wealth accumulation, estate and retirement planning, and investment implementation—where any regulated advice or execution is provided only by licensed entities. Our role is to make the journey clearer, safer, and easier to navigate.

Whether you’re starting your savings plan or managing more complex needs, HWG’s client-first approach emphasises transparency, plain language, and solutions aligned to your goals—without implying or providing regulated advice from HWG itself.

Discover How HWG Can Help You Manage Your Wealth:

- Estate & retirement planning education for different life stages.

- Investment implementation delivered by appropriately licensed entities, aligned to your goals and risk tolerance.

- Ongoing reviews & updates so your plan can evolve with changes in life and markets.

Contact HWG Malaysia Today:

Address: 42, Jalan BM1/2, Taman Bukit Mayang Emas, 47301 Petaling Jaya, Selangor

Email: customerservice@hwg.asia

Phone: 03-5569 9834

Inquiry: Contact Us

Visit HWG Malaysia’s Social Media Profiles:

Website: https://www.hwg.asia/

Facebook: https://www.facebook.com/hwg.asia

LinkedIn: https://www.linkedin.com/company/hwgasia/

Download the HWG Apps (Available on the Play Store and App Store)!

HWG Hub: HWG Hub (For Internal Partner Use Only)

HWG Go: Available on the Play Store and App Store

Disclaimer:

This article, published on this website, may be written or contributed by subject-matter experts or external writers. They are intended for general information and educational purposes only. HWG does not guarantee the accuracy, completeness, or timeliness of the information provided. Please note that the products, services or solutions in these articles may not be offered or provided by HWG. HWG shall not be held responsible or liable for any loss, damage, or issues arising from the use of, or reliance on such information.