Most Malaysians rely on EPF as the core of retirement savings, with PRS and other investments used to add flexibility and growth. Choosing a mix that fits your income, risk tolerance, and timeline can reduce dependence on any single source. (General information only.)

EPF Malaysia Retirement Savings Explained: Contributions, Dividends, and Withdrawal Rules

EPF Malaysia retirement savings serve as the main pillar for private sector employees. Both employee and employer contribute monthly based on salary. The current combined contribution rate reaches up to 23 percent for most workers. This structure forces disciplined saving across an entire working life.

EPF invests funds across bonds, equities and property. Annual dividends averaged between 3 percent and 6 percent over the past decade. The fund also guarantees a minimum dividend of 2.5 percent for conventional savings. This provides stability during market downturns.

Withdrawals follow strict rules tied to age, health and housing needs. Full retirement withdrawals start at age 55. Partial access earlier supports education, housing and medical needs. This balance protects retirement savings while allowing limited flexibility.

EPF Voluntary Contributions for Self-Employed and Gig Workers in Malaysia

EPF Malaysia retirement savings extend beyond salaried workers. Self-employed individuals and gig workers join through voluntary schemes like i Saraan. Contributors receive government incentives based on annual contributions. Recent updates increased incentives up to RM600 per year for eligible members.

Voluntary contributions allow top ups as low as RM10. Annual contribution limits reach RM100000. This suits individuals with irregular income. Consistent monthly deposits improve compounding over time.

Tax relief strengthens the appeal of EPF. Contributors receive personal tax relief up to RM7000 per year. Dividends remain tax-exempt. These features improve net returns compared with taxable investment products.

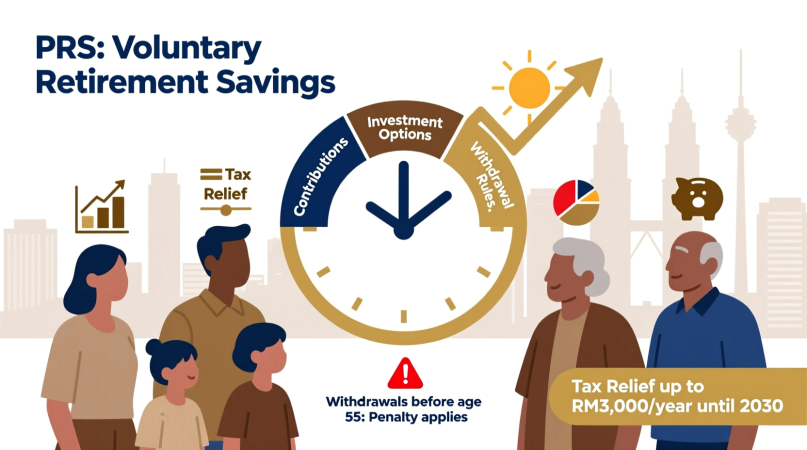

What Is the Private Retirement Scheme (PRS) in Malaysia and How Does It Work?

The PRS retirement plan in Malaysia works as a voluntary long-lasting savings scheme. PRS supplements EPF rather than replacing it. Individuals choose funds managed by private providers approved by regulators. Contributions remain flexible with no fixed monthly requirement.

PRS funds invest across equities, bonds and money market instruments. Risk profiles range from conservative to growth-focused. Younger investors often select growth funds for higher enduring returns. Older contributors shift toward balanced or conservative funds.

Tax incentives drive PRS adoption. Contributors receive tax relief up to RM3000 per year until 2030. Withdrawals before age 55 trigger penalties on the withdrawn amount. This discourages early access and protects retirement goals.

PRS Retirement Plans in Malaysia: A Flexible Option for High, Variable and Young Income Earners

The PRS retirement plan in Malaysia suits individuals who exceed EPF contribution limits. High-income earners use PRS to increase total retirement savings efficiently. Business owners and freelancers benefit from flexible contribution timing. This structure adapts to income fluctuations.

Young professionals gain from long investment horizons. A 30 year old contributing RM300 monthly with 6 percent annual returns accumulates over RM300000 by age 60. This excludes tax relief benefits. The result strengthens retirement income without relying solely on EPF.

PRS also supports Shariah compliant investing. Contributors select Shariah funds aligned with personal beliefs. This expands access for investors seeking ethical investment structures.

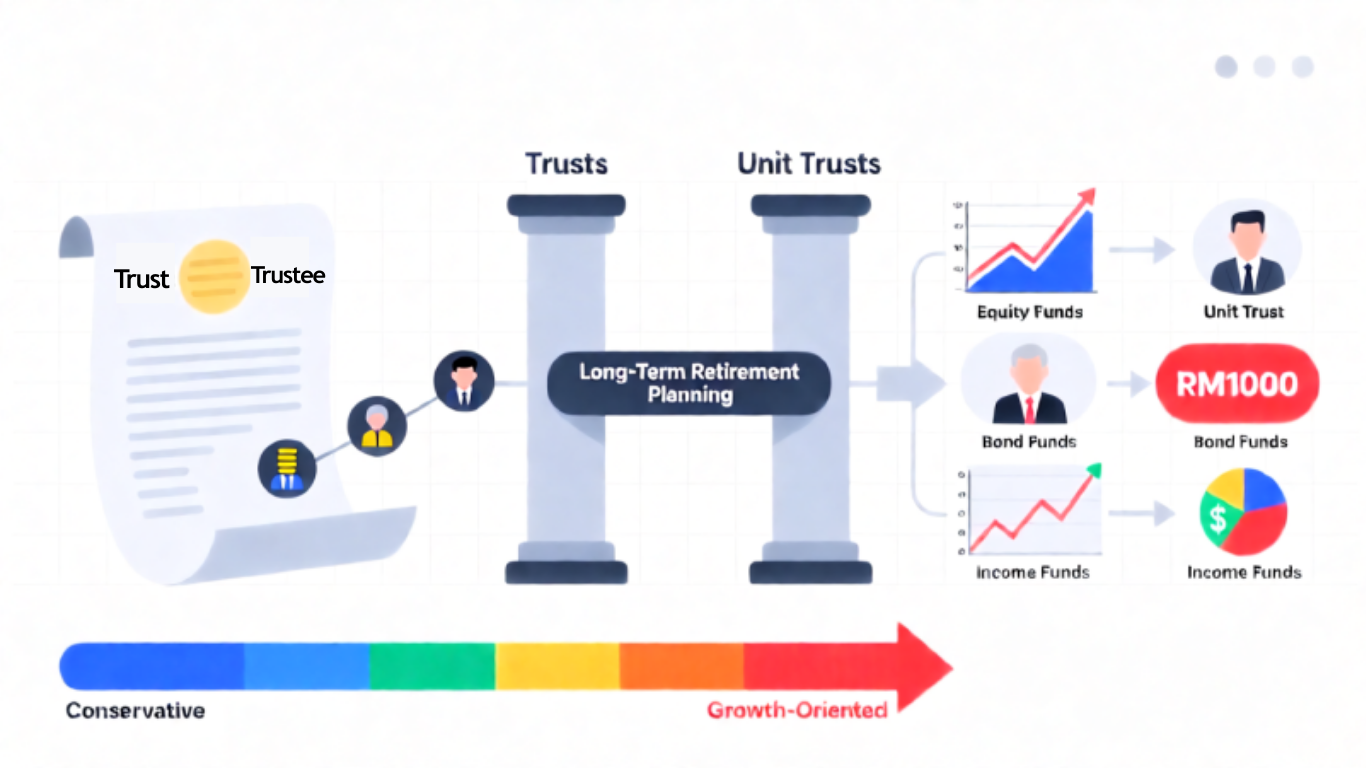

Trusts and Unit Trusts as Retirement Investment Options in Malaysia

Trusts represent a broader category within retirement investment options in Malaysia. Unit trusts allow pooled investments managed by professional fund managers. Investors gain diversification across sectors and markets. Entry amounts often start below RM1000.

Unit trusts support a medium to lasting focusing on retirement goals. Equity-based funds target higher returns over time. Bond and income funds suit conservative investors seeking stability. Switching funds adjusts risk exposure as retirement approaches.

Trust structures also support estate planning. Trust deeds define beneficiaries and distribution rules. This helps manage wealth transfer across generations. Trusts require discipline and periodic review to remain aligned with retirement goals.

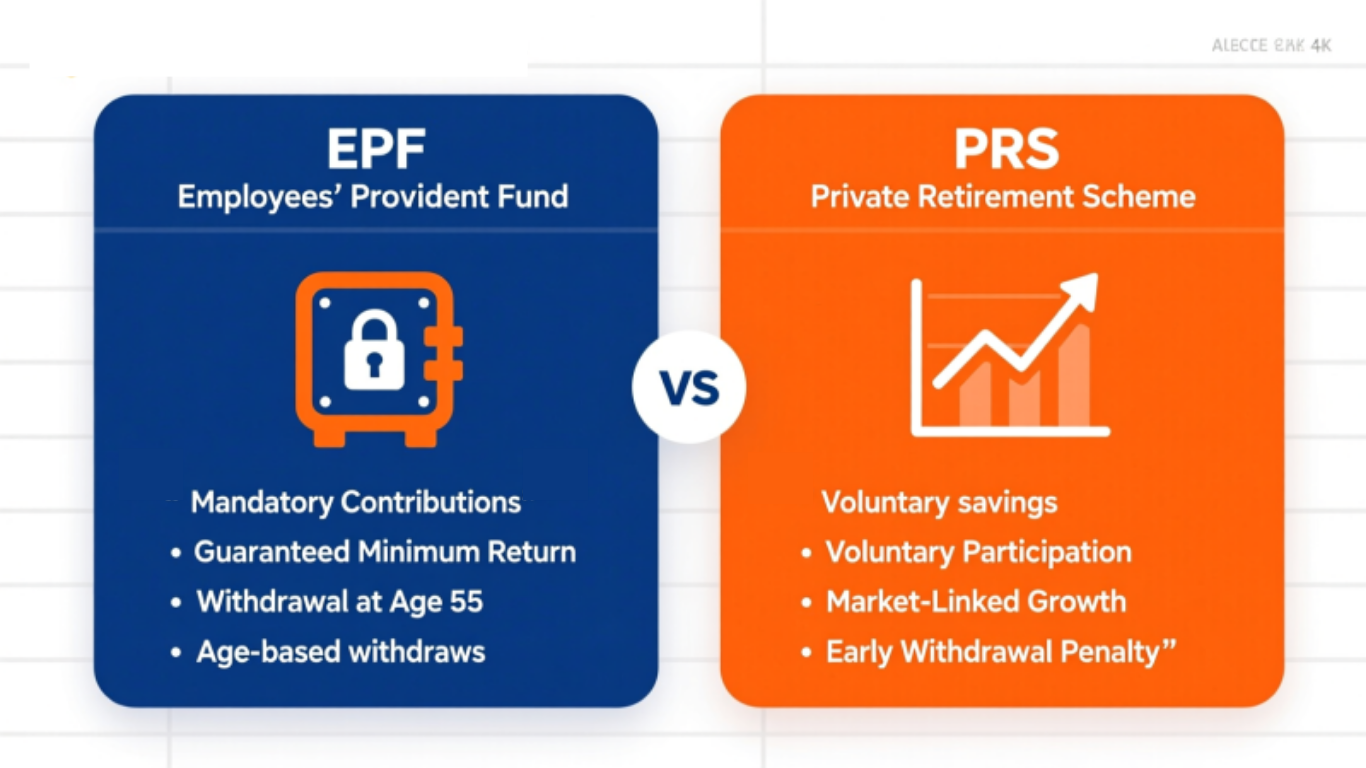

EPF vs PRS in Malaysia: Key Differences in Structure, Returns and Withdrawal Rules

EPF vs PRS Malaysia retirement savings differ across structure, returns and access. EPF enforces mandatory savings for employees. PRS relies on voluntary discipline. This distinction affects consistency and outcomes.

EPF offers stable returns backed by regulation. PRS exposes savings to market performance without guarantees. Higher risk may produce higher returns. This suits investors with longer horizons.

Liquidity differs significantly. EPF restricts withdrawals until specific ages. PRS penalizes early withdrawals. Both systems protect retirement funds by limiting access. Combining both balances stability and growth.

How Much Retirement Savings Should You Have in Malaysia?

Retirement savings options in Malaysia align with income replacement targets. Financial planners often recommend replacing 70 percent to 80 percent of final income. EPF introduced retirement adequacy benchmarks to guide members.

EPF sets three tiers. Basic savings target RM390000 at age 55. Adequate savings target RM650000. Enhanced savings target RM1300000. These figures support different lifestyle expectations.

For example, a retiree spending RM3000 monthly requires RM36000 annually. Over 20 years, this equals RM720000 excluding inflation. Combining EPF PRS and investments helps close gaps. Early planning reduces pressure later.

What Are The Best Retirement Plans in Malaysia?

The best retirement plans in Malaysia depend on income stability, age and risk tolerance. EPF suits individuals seeking structured and stable growth. PRS supports those aiming to increase savings beyond mandatory limits. Trusts suit investors comfortable managing market risk.

A balanced approach works best. EPF builds the foundation. PRS adds flexibility and tax efficiency. Trusts and unit trusts add diversification. This mix reduces dependence on one source.

Regular reviews improve outcomes. Adjust contributions when income rises. Shift asset allocation as retirement nears. These actions improve high security.

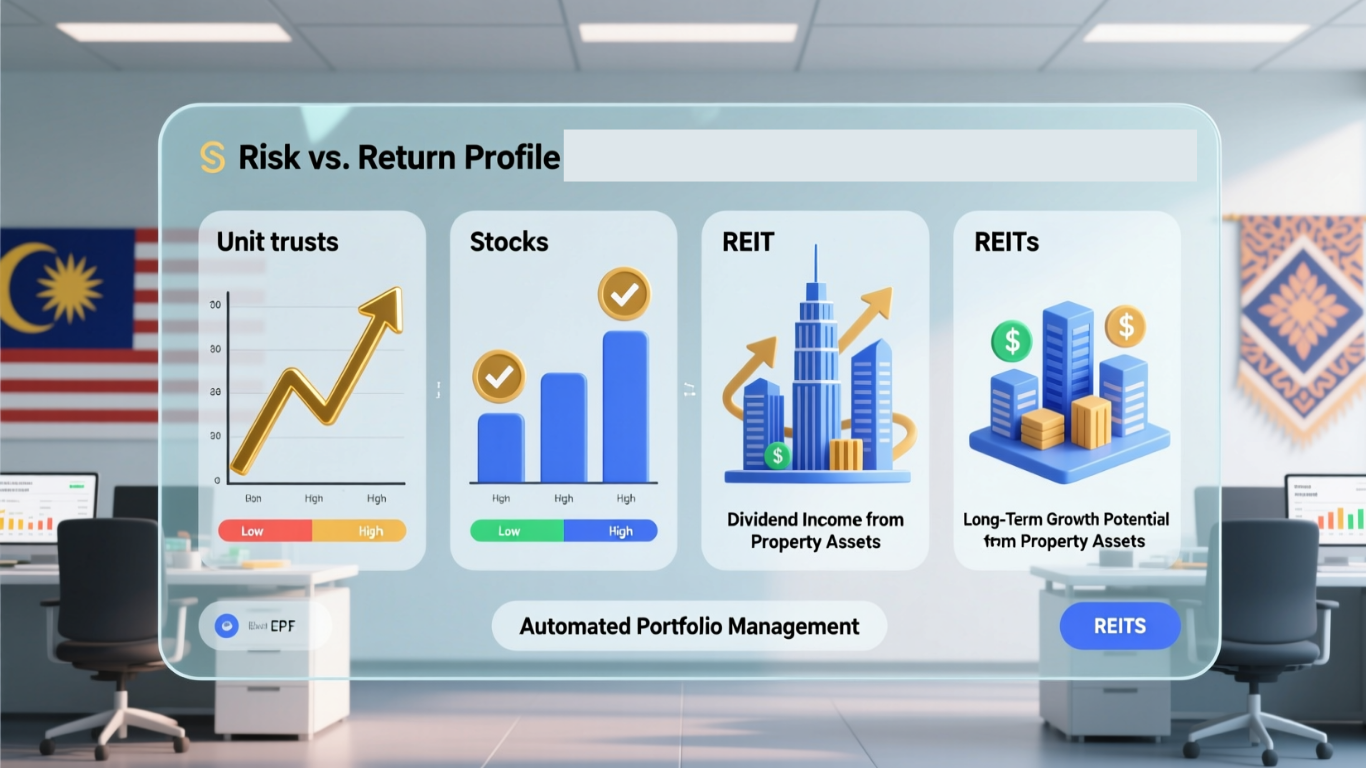

What Are The Options for Retirement Savings in Malaysia?

Retirement savings options in Malaysia extend beyond EPF and PRS. Common options include unit trusts, stocks, bonds and REITs. Each carries different risk and return profiles.

Stocks offer higher growth potential over long periods. Bonds provide income and stability. REITs deliver regular dividends tied to property assets. Combining assets smooths volatility.

Digital investment platforms simplify access. Robo advisors manage diversified portfolios based on risk profiles. These platforms suit beginners seeking low cost entry. Discipline and consistency remain key.

Practical Steps to Improve Retirement Savings Options in Malaysia

Start by calculating your current savings across all retirement-related accounts, including EPF, private retirement schemes and other long-term investments. Compare this total with EPF adequacy targets to understand whether you are on track for a sustainable retirement. Identifying any shortfall early is critical, as it gives you more time to take corrective action. Once gaps are clear, adjust your contribution levels gradually. Small, incremental increases help prevent sudden lifestyle disruptions while still improving outcomes.

Automating monthly contributions is one of the most effective ways to stay consistent. Treat retirement savings as fixed expenses, similar to rent or utility bills, so contributions are prioritised before discretionary spending. Whenever possible, increase contributions during bonus periods, salary increments or unexpected income spikes. These moments provide opportunities to strengthen retirement savings without affecting day-to-day cash flow. At the same time, avoid early withdrawals unless necessary, as they significantly reduce the power of compounding over time.

Seek professional advice when needed, especially if your financial situation becomes more complex. Retirement calculators and planning tools can help estimate future income needs and test different contribution scenarios. Review your progress at least once a year to ensure you remain aligned with your retirement goals and adjust your strategy as circumstances change. Over time, small and consistent actions compound into meaningful results, building greater financial security and confidence for retirement.

Closing thoughts on retirement savings options in Malaysia

Malaysia offers a structured base (EPF), a flexible top-up (PRS), and additional tools (unit trusts/trust structures) to tailor a plan. Early planning, steady contributions, and periodic reviews do more for retirement security than any one “best” product.

Unlock Your Wealth Management with HWG Asia – Malaysia’s Leading Wealth Management Partner

Explore more with HWG

HWG is a Malaysia-based wealth education and marketing support platform that partners with licensed financial institutions. We share practical insights and coordinate services delivered by appropriately licensed entities within our group (e.g., Maxima Advisory).

We focus on education and coordination across topics like wealth accumulation, estate and retirement planning, and investment implementation—where any regulated advice or execution is provided only by licensed entities. Our role is to make the journey clearer, safer, and easier to navigate.

Whether you’re starting your savings plan or managing more complex needs, HWG’s client-first approach emphasises transparency, plain language, and solutions aligned to your goals—without implying or providing regulated advice from HWG itself.

Discover How HWG Can Help You Manage Your Wealth:

- Estate & Retirement planning solutions for every life stage.

- Investment management strategies are designed to maximize returns while managing risk. (it is delivered by appropriately licensed entities)

- Ongoing support with regular reviews to ensure your plan evolves with you.

Contact HWG Malaysia Today:

Address: 42, Jalan BM1/2, Taman Bukit Mayang Emas, 47301 Petaling Jaya, Selangor

Email: customerservice@hwg.asia

Phone: 03-5569 9834

Inquiry: Contact Us

Visit HWG Malaysia’s Social Media Profiles:

Website: https://www.hwg.asia/

Facebook: https://www.facebook.com/hwg.asia

LinkedIn: https://www.linkedin.com/company/hwgasia/

Download the HWG Apps (Available on the Play Store and App Store)!

HWG Hub: HWG Hub (For Internal Partner Use Only)

HWG Go: Available on the Play Store and App Store

Disclaimer:

This article, published on this website, may be written or contributed by subject-matter experts or external writers. They are intended for general information and educational purposes only. HWG does not guarantee the accuracy, completeness, or timeliness of the information provided. Please note that the products, services or solutions in these articles may not be offered or provided by HWG. HWG shall not be held responsible or liable for any loss, damage, or issues arising from the use of, or reliance on such information.