Early retirement simply means leaving full-time work before Malaysia’s statutory minimum retirement age (currently 60). Whether your target is 55, 50, or earlier, success depends on replacing employment income with reliable, planned cash flows—while accounting for taxes, healthcare, inflation, and longevity. This article breaks down the financial instruments that can support early retirement in Malaysia.

Early Retirement Definition?

Early retirement is, by definition, the act of retiring from employment before reaching the legal retirement age, especially if the terms are favorable. When someone quits their job before the standard statutory retirement age, it’s known as early retirement. Unplanned early retirement puts more strain on the retirement plan since the person has fewer assets that can endure longer to support the person’s life.

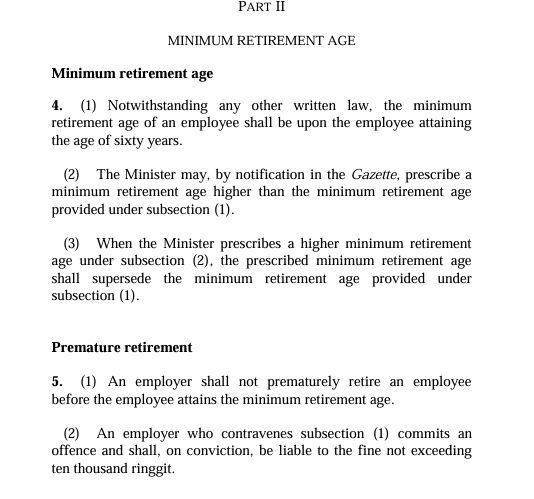

Latest, the standard minimum retirement age in Malaysia was set to 60 according to the Minimum Retirement Age Act 2012. However, there is a circulating news that the current government is reviewing the possibility of raising it to 65. This review is in response to the country’s aging population and is expected to be discussed in the upcoming 2026 budget. While the age remains 60, discussions are underway, and it may change in the future. In other words, early retirement means stopping full-time work before this benchmark and relying on personal assets, investments, or alternative income streams.

For example:

- At age 55, EPF savings become partially accessible under current rules.

- Some Malaysians target 50 or younger if they have business proceeds, property income, or structured investment withdrawals.

To retire early in Malaysia, your plan must account for several years of income gap before government benefits or full EPF access become available. You need to think through tax impact, healthcare, inflation, and lifestyle maintenance over 30 or more years.

Know Your EPF Amounts and Withdrawal Rights

EPF is the main retirement savings tool for many working Malaysians. Under current rules, partial EPF withdrawals start at age 50, and full withdrawals can begin at age 55.

If you retire before 55:

- You cannot access your EPF Account 1, except under specific hardship schemes.

- You may only withdraw from Account 2 for housing, education, or medical needs.

- EPF i-Invest lets you channel a portion of Account 1 into approved funds for higher potential returns, but these funds remain locked in until 55 unless you’re eligible under early access schemes.

Planning for early retirement means preparing to bridge income until your EPF funds are fully available. EPF can still be part of your investment growth, but not your cash flow before 55 unless timed precisely.

However, if you plan to withdraw your retirement savings EPF before it matures, you need to bear in mind that the amount might not be enough to support your retirement period and live comfortably. How much money do you actually need to retire comfortably in Malaysia? The EPF sets a minimum retirement target of RM240,000 by age 55. Many Malaysians struggle to reach this figure. A DOSM survey found that most households only have savings to last 1 to 4 months without income.

If you retire at 55 with RM240,000 and spread the amount across 20 years, you get RM1,000 a month. This raises a question. Does this amount support real living costs, especially with factors that reduce spending power over time? Let’s look at what affects this.

Read More: Retirement Planning Malaysia: How Much Money Do You Need to Retire Comfortably in Malaysia? – HWG Asia

Build Alternative Income Streams from Early

To retire early, it is a compulsory instrument to have assets that pay you regularly. Here are the most common sources of retirement income Malaysians use other than EPF:

- Dividend-Paying Stocks and REITs

Invest in Bursa Malaysia-listed companies or real estate investment trusts with a proven history of stable dividends. Public Bank, Maybank, and Axis REIT are examples often cited by income investors.

- Unit Trusts and Robo-Advisors

Licensed platforms under the Securities Commission Malaysia now offer Digital Investment Management (DIM) options. You can select goal-based portfolios, opt for Shariah-compliant funds, and automate contributions using DuitNow. Over time, these portfolios grow and provide withdrawals aligned with your retirement timeline

- House, Room, or any Property Rental Income

Invest in residential or commercial property in growth areas like industrial states like Johor Bahru, Penang, Klang Valley, and other states as long as it creates money growth. Make sure rental yield covers your mortgage and provides positive cash flow. Factor in vacancy risk and maintenance costs.

- Business Exit or Passive Business Models

Some early retirees build up a business, sell it, or convert it into a passive income model. This might include franchising, licensing, or transferring to a family trust.

Plan for multiple income streams to manage risk. Relying on a single source, especially in volatile markets, adds stress and uncertainty to early retirement.

Secure Private Medical Coverage Before Retirement

Private healthcare costs in Malaysia continue to rise. Once you retire, your employer-provided coverage usually ends. Early retirees must prepare to self-fund medical insurance.

Here’s what you can do:

- Buy a standalone medical card early. Premiums are lower if you purchase before age 45.

- Choose plans with guaranteed renewal and no lifetime limit.

- Consider critical illness coverage, especially if you’re the main financial decision-maker in your household.

Some platforms offer insurance recommendations based on your health profile and coverage needs. Keep premiums sustainable so they do not disrupt your retirement cash flow later.

Understand the Tax Impact of Early Retirement in Malaysia

Malaysia has no capital gains tax on shares or mutual fund income. Dividend income is also tax-exempt for individuals. This makes early retirement income from investments tax-efficient.

However, be aware of:

- Rental income taxation: You must report it, but you can deduct related expenses.

- Business income: If you run a side business post-retirement, register and file accordingly.

- EPF withdrawals: These are tax-free if withdrawn under approved conditions at age 50 or 55.

To reduce future taxes, consider these steps:

- Use a holding company to manage rental or dividend flows.

- Assign insurance proceeds or business shares through a private trust structure.

- Split income across family members through estate or succession planning.

Tax planning is essential for early retirees who want to stretch capital across decades.

Use a Retirement Budgeting Rule That Matches Reality

Malaysians can refer to the “4% Rule for Withdrawals in Retirement”, which assumes a 4 percent withdrawal rate from investments will last 30 years. In Malaysia, this is a useful benchmark, but it needs local adjustment due to inflation, currency, and healthcare differences.

- Calculate total annual spending (including housing, food, travel, and insurance).

- Add a 5–6 percent inflation factor for medical and food costs.

- Plan to withdraw 3.5 to 4 percent of your portfolio annually.

- Rebalance every year using automated tools or a wealth manager.

If your annual spending is RM60,000, you need an investment portfolio of RM1.5 to RM1.7 million at a 4 percent rate. Adjust upward if you expect higher living expenses or want to leave assets to children.

Estate Planning Still Matters Before Age 60

Early retirees often skip estate planning, assuming it is only for older people. That is a mistake.

Use the years before 60 to:

- Create a simple will or hibah to allocate your assets.

- Set up a trust if you want a structured distribution to children or to protect assets from disputes.

- Name a trusted executor or trustee.

- Consolidate insurance and investment account instructions.

If you are self-managing wealth instead of relying on EPF alone, your portfolio becomes part of your estate planning. Plan its transfer before unexpected events delay or disrupt access.

Estate and retirement planning at Holistic Wealth Group (HWG) focuses on long-term stability and clear asset distribution for future generations. HWG highlights the value of preparing early to maintain financial security and support smooth transfers of assets.

Services include will execution, custodial support, estate administration, and trust execution. These services form a structured approach to building a practical and organized retirement and estate plan.

Contact HWG Malaysia | Get in Touch 2025/2026

Why Wealth Management Helps Early Retirees Stay Independent

Even if you are financially ready, early retirement often fails due to poor planning, emotional spending, or unanticipated shocks. Partnering with a wealth management firm like HWG can improve long-term confidence.

- Regular reviews of your investment performance and withdrawal strategy.

- Access to licensed financial planners who understand Malaysia-specific rules.

- Legacy planning tool, including trust structures, MBO exit planning, and keyman coverage for business owners

Good wealth management keeps your early retirement plan aligned with your lifestyle, family needs, and financial goals without daily stress.

Final Thoughts: Early Retirement in Malaysia Is Possible With Planning

Early retirement in Malaysia depends less on luck and more on math and structure. Start by calculating your monthly needs, build investment income that pays those needs, prepare for medical and tax costs, and protect your estate.

Use your 30s and 40s to build the plan. By 50, the numbers should tell you whether early retirement is possible. By 55, execution should be in place.

For help, speak with a financial planner or wealth management firm with experience in early retirement planning in Malaysia.

Unlock Your Wealth Management with HWG Asia – Malaysia’s Leading Wealth Management Partner

You can always explore more at HWG!

HWG is a wealth management firm in Malaysia, offering wealth accumulation services tailored to Malaysian needs. From wealth advisory, estate, and retirement planning to investment management (it is delivered by appropriately licensed entities), we provide expert advice and secure, personalized solutions that empower you to achieve wealth and financial security.

Whether you’re a young professional just starting to save and invest or a high-net-worth individual seeking advanced wealth strategies, HWG’s client-first model ensures that your goals are met with integrity and expertise.

Discover How HWG Can Help You Manage Your Wealth:

- Estate & Retirement planning solutions for every life stage.

- Investment management strategies are designed to maximize returns while managing risk (it is delivered by appropriately licensed entities).

- Ongoing support with regular reviews to ensure your plan evolves with you.

Contact HWG Malaysia Today:

Address: 42, Jalan BM1/2, Taman Bukit Mayang Emas, 47301 Petaling Jaya, Selangor

Email: customerservice@hwg.asia

Phone: 03-5569 9834

Inquiry: Contact Us

Visit HWG Malaysia’s Social Media Profiles:

Website: https://www.hwg.asia/

Facebook: https://www.facebook.com/hwg.asia

LinkedIn: https://www.linkedin.com/company/hwgasia/

Download the HWG Apps (Available on the Play Store and App Store)!

HWG Hub: HWG Hub (For Internal Partner Use Only)

HWG Go: Available on the Play Store and App Store

Disclaimer:

This article, published on this website, may be written or contributed by subject-matter experts or external writers. They are intended for general information and educational purposes only. HWG does not guarantee the accuracy, completeness, or timeliness of the information provided. Please note that the products, services or solutions in these articles may not be offered or provided by HWG. HWG shall not be held responsible or liable for any loss, damage, or issues arising from the use of, or reliance on such information.